The foundation and the basis for the provision of a safe and efficient payments domain is the development of a sound and appropriate legal framework. As the payments domain evolves and more players enter the field, new business models are introduced, which blur the line of traditional payment products. Along with this, the impact these players have on the stability of the financial markets also increase. As such, there is an increasing need for a modernized and strengthened regulatory framework in order to ensure stability of the financial market as well to ensure the prudent behaviour of payment service providers.

Accordingly, MMA is working concurrently on developing a comprehensive and harmonious legal framework, in line with the objectives of promoting innovation and competition in the market, while assuring the public of the safety and efficiency of payment systems.

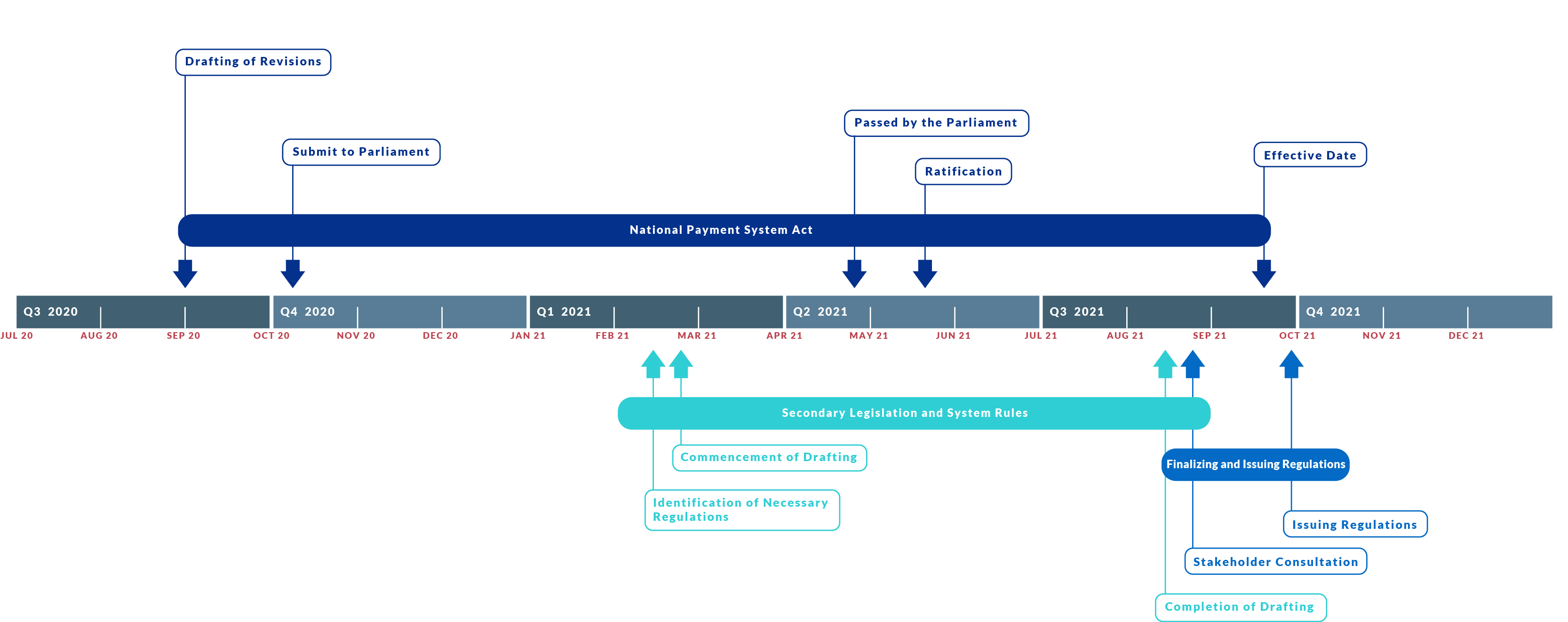

The National Payment Systems Act will become effective in September 2021. This Act will be the key legislation that will provide the relevant legal basis for the implementation of a national payment system and to license, regulate and oversee systematically important financial market systems.

With the implementation of the MPSD project, significant changes are expected in the payments industry as it will provide a new window of opportunity for the potential players to enter to the industry offering modern and innovative digital financial solutions.

In order to ensure that the regulations are up to par with the changing conditions of the payments domain, secondary legislations are being drafted under this Act – inclusive of licensing guidelines and regulations of the Payment Systems, Payment Service Providers, E-money Issuance, Data Privacy regulation, Consumer Protection regulations. Aspects of oversight, cyber security, electronic signature, to broadly name a few areas, would also be encompassed within the secondary legislation.

Moreover, as a response to the evolving payments landscape, the secondary legislations will move towards an activity-based approach, with a focus on risk assessed entry into the payments field. Such an approach will not only result in fostering of healthy competition amongst banks and non-bank payment service providers but will also have trickle down impacts on the end-customers themselves – through safer, efficient, and innovative financial services.

The secondary legislations are expected to be published during the last quarter of 2021, prior to the go-live of the Instant Payment System.

Timeline

Updated on June 2021